Artificial Intelligence at U.S. Bank – Two Current Use Cases

U.S. Bank is the fifth largest bank in the United States by total assets. Traded on the NYSE (symbol: USB), the company has a market capitalization of approximately $67 billion. In its 2021 annual report, U.S. bank reported a net income of $8 billion on $22.8 billion in revenue. In the same report, the CEO cites nearly 70,000 employees.

On a separate page of its website, U.S. Bank states it has identified and continues to pursue” many AI initiatives. U.S. Bank lists 11 AI “focus areas,” most of which are common AI use cases for banking, including anomaly fraud detection, interpreting images and language, improving customer relationships, and machine learning with graphs.

The company’s annual report does not mention any specific investments in AI. A recent LinkedIn search lists 277 data scientists at the company.

How U.S. Bank’s use of AI supports its business goals is exemplified through two specific use cases:

- Automated savings and investments: U.S. Bank’s ‘Pay Yourself First’ application uses predictive analytics to analyze cash flow patterns and auto-deposit disposable funds into savings or investment accounts.

- Increasing lead conversion: U.S. Bank uses machine learning and predictive analytics to increase the lead conversion rates of small business customers.

First, let’s look at how U.S. Bank uses AI to offer an automated savings and investments option.

Use Case #1: Using AI To Automate Savings and Investments

As stated in a recent article posted on U.S. Bank’s blog about the firm’s ‘Pay Yourself First’ app, when it comes to saving money, “the tricky part is deciding how much.”

U.S. Bank notes that this problem was magnified during the early periods of the pandemic, citing Federal Reserve data supposedly showing Americans saving money “at a record pace” compared to pre-pandemic savings levels. (The citation to the Fed link is broken, but data from the Bureau of Economic Analysis seems to validate U.S. Bank’s claims.)

Trying to turn a challenge into a business opportunity, U.S. Bank then partnered with Personetics, an Israeli financial technology software company, to achieve its goals. Per its website, Personetics specializes in “data-driven personalization and customer engagement solutions.” The company states on its website that it uses AI to analyze financial data in real-time.

Last year, Personetics announced it had patented a solution to help U.S. Bank’s customers save or invest based on cash flow patterns.

Personetics did not provide information on how they trained their model. However given the model’s purpose, the model’s training involved labeling and inputting vast amounts of customer financial/transactional data. The company’s data team may also use historical discretionary income, savings, and investment data.

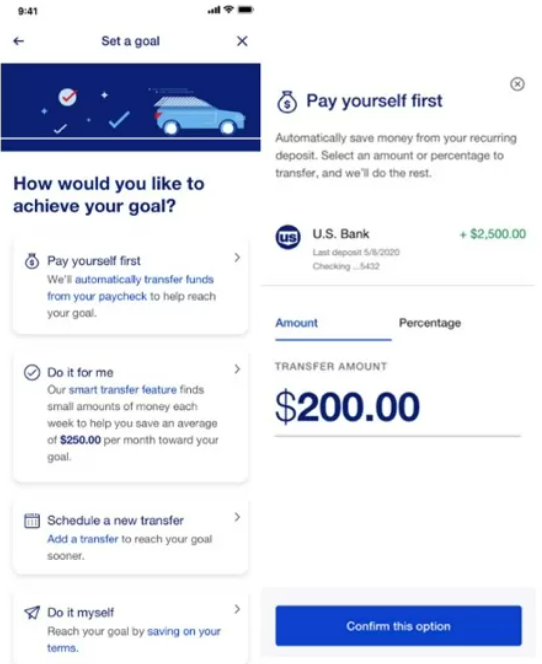

On the user side, customers enter the amount they’d like to save each pay period into the application as either a desired dollar amount or percentage of income. The application’s AI algorithms then calculate the savings amount based on expense patterns until the next projected income deposit and put the money into the designated savings or investment accounts.

Customer Input Screen. (Source: Personetics)

As the application is relatively new – it was released in 2021 – more time is needed to properly judge outcomes for the application. Of course, much information regarding outcomes has not yet been made public.

Use Case #2: Increasing Lead Conversion

According to its partner Salesforce, U.S. Bank’s prior CRM ran on separate databases, with each requiring separate updates and upgrades. This fragmented system results in less actionable customer data to salespeople and, as a result, subpar lead conversion rates and revenue. Salesforce claims that it came up with a way to unify the disparate customer data, increasing lead conversion and driving revenue.

Per Salesforce, the best solution for U.S. Bank was their product Salesforce Einstein, which the company claims is “the first comprehensive AI for CRM.” According to the Salesforce website, the software works by using “data science and machine learning to discover … patterns in lead conversion.” The company states that the software predicts lead conversion for each customer based on data from previously-converted leads. The algorithm scores the leads using “lead fields.” Examples of this scoring data may include:

- Customer’s industry

- Customer location

- Department

- Annual revenue

- Lead Source

According to the customer support literature available on the company’s website, its algorithm creates a predictive model for the organization, which recalculates the data every ten days. For organizations lacking the initial data for lead conversion, Salesforce uses a “global model” trained off anonymous customer data. Once the client accumulates enough lead data, Salesforce tells customers the algorithm will calculate a more client-specific scoring model with more accurate results.

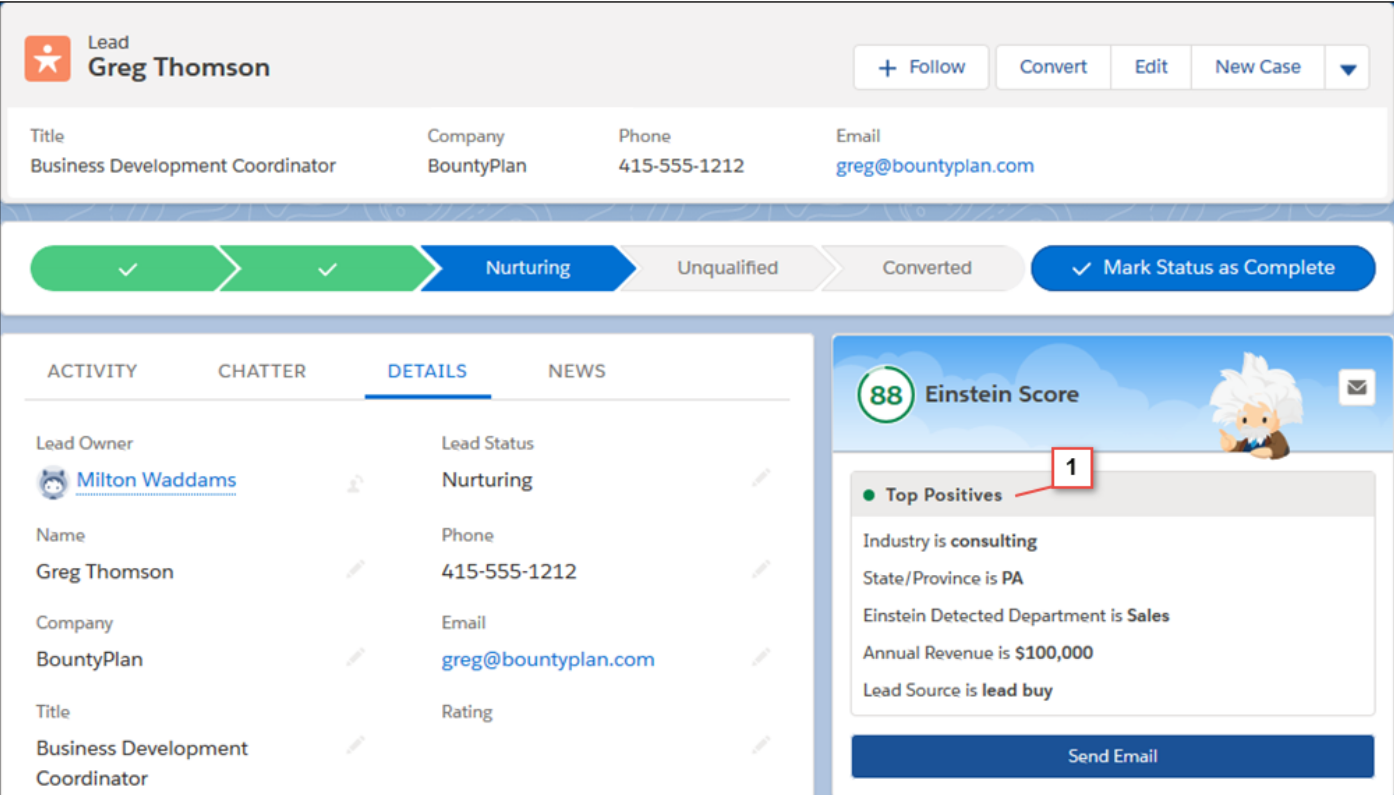

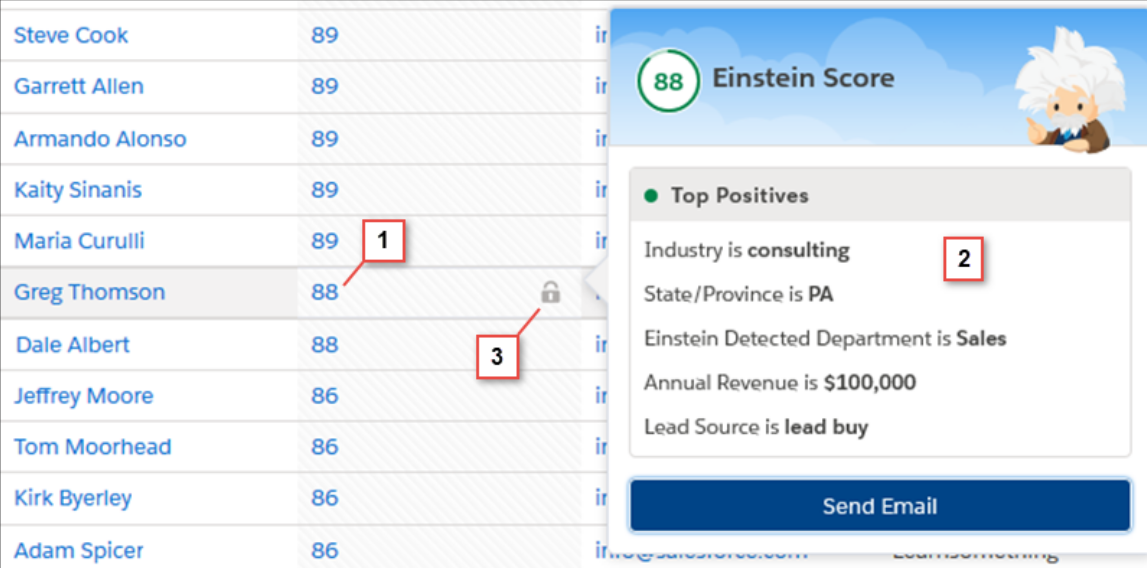

On the end-user side, the sales agent sees the lead’s name, job title, company, contact information, and lead status. The “Einstein Score” is listed below this data, along with the score’s contributing factors (see the top screenshot below).

Customer Detail Screen. Score factors on the right. (Source: Salesforce)

Besides the lead screens, the user can access – and filter – customer dashboard with the following data:

- Average lead score by source: Lead sources that are receiving the highest scores from Einstein Lead Scoring.

- Conversion rate by lead score: Conversion data is bucketed in a way that conversion rate and lead score are designed to correlate. (For example, leads with scores in the 80-100 range should have a higher conversion than those in the 20-40 range.)

- Lead score distribution: Lead score buckets that compare converted versus not-converted leads.

Regarding business outcomes for U.S. Banks, Salesforce reports a “lift in lead conversion” of 2.35 times. In a Salesforce blog post, it is reported that the software was able to score 4.5 million leads in two hours.

Machine learning algorithms are claimed to have uncovered previously undetectable customer insights, giving the example that “a mortgage owner is more likely to increase assets under management if they had a credit card.”